|

Current Economic Statistics and Review For the

Week | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Recent Trends in Saving and

Investment: An Analysis*

| |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Table 1: Domestic Saving, Investment and Capital Inflow Ratios During Plan Periods |

|||

|

Plan Period |

As Percentage of GDP at Current Market Prices |

||

|

Gross Domestic Saving Rate |

Gross Investment Rate |

Net Capital Inflow |

|

|

Eighth Plan (1992-93 to 1996-97) |

23.1 |

24.4 |

1.3 |

|

Ninth Plan (1997-98 to 2001-02) |

23.6 |

24.3 |

0.7 |

|

Tenth Plan (2002-03 to 2006-07) |

31.9 |

32.1 |

1.2 |

|

Eleventh Plan Targets (2007-08 to 2011-12) |

34.8 |

36.7 |

2.1 |

|

Source: Planning Commission (2008): Eighth Five Year Plan 2007-12 (Vol.I), p.27. |

|||

Quantum Leap after the Tenth Plan

|

Table 2: Domestic Saving and Investment and Capital Inflow as Percentages of GDP at Current Market Prices |

|||

|

Year |

Gross Domestic Saving Rate |

Gross Capital Formation Rate |

Net Capital Inflow |

|

1999-2000 |

24.8 |

25.9 |

1.1 |

|

2000-01 |

23.7 |

24.3 |

0.6 |

|

2001-02 |

23.5 |

22.8 |

(-) 0.7 |

|

2002-03 |

26.3 |

25.2 |

(-) 1.1 |

|

2003-04 |

29.8 |

27.6 |

(-) 2.2 |

|

2004-05 |

31.7 |

32.1 |

0.4 |

|

2005-06 |

34.2 |

35.5 |

1.3 |

|

2006-07 |

35.7 |

36.9 |

1.2 |

|

2007-08 |

37.7 |

39.1 |

1.4 |

|

Source: CSO (2009): Quick Estimates of National Income, Consumption Expenditure, Saving and Capital Formation 2007-08, January |

|||

The year 2002-03, the first year of the tenth plan, became the turning point in the saving and investment scenario (Table 2). The saving rate jumped from 23.5% in 2001-02 to 26.3% in 2002-03 and thereafter it has not looked back; there has been an addition of about two percentage points in each of the years for the next five years until 2007-08, when the saving rate touched 37.7% - a rate close to the 40% rate achieved by many south-east Asian countries, particularly China. It has indeed been a commendable achievement, for which the reasons are found in the developments not only in the macro economy of India but also in the global economy (more of it later).

Even as domestic saving

rate galloped, there has occurred a quantum leap in the country’s

investment rate. For sometime in the initial period of the high saving

phase (2001-02 to 2003-04) when rapid increases in foreign capital flows

took place and domestic savings began to expand, the domestic investment

rate could not catch up with the bulge in savings. As a result, there was

the unhealthy spectacle of the country’s current account getting into a

situation of surplus, that is, the counterpart of the negative capital

inflow. As shown in Table 2, the three year period 2001-02 to 2003-04

experienced negative capital inflows ranging from (-) 0.7% to (-) 2.2% of

GDP. That is, a saving-scarce economy like that of India experienced a

situation of net capital outflow. The reasons were not far to seek. The

root reason was the rapid bulge in capital inflows which contributed to

the phenomenal increases in the country’s foreign exchange reserves (Table

3). The bulge began precisely in 2002-03 which is associated with a number

of positive developments in the country’s macroeconomy thereafter

including the vast increases in domestic saving and investment. The

foreign exchange reserves, which had increased by $11.83 billion (Rs

66,831 crore) during 2001-02, expanded more rapidly thereafter by US

$21.99 billion (Rs 97,432 crore) in 2002-03 and 36.86 billion (Rs 128,659

crore) in 2003-04. Such sudden increases in foreign reserves could not be

absorbed by expanding investment in the economy contemporaneously and

hence these were current account surpluses or negative net capital inflows

for three years until 2003-04. But, by then, the country’s domestic

investment rate had begun to improve rather rapidly, though not

commensurate with the capital inflows or with the increases in the

domestic saving rates. The gross capital formation (GCF) rate jumped from

22.8% of GDP in 2001-02 to 25.2% in 2002-03 and further to 27.6% in

2003-04. But, after 2003-04, the investment rates have overtaken the

savings rates, thus absorbing the foreign capital inflow albeit

partly to finance current account deficits and increased investment. Thus,

the GFC rate has steadily risen to as high a figure as 39.1% in 2007-08.

Even as domestic saving

rate galloped, there has occurred a quantum leap in the country’s

investment rate. For sometime in the initial period of the high saving

phase (2001-02 to 2003-04) when rapid increases in foreign capital flows

took place and domestic savings began to expand, the domestic investment

rate could not catch up with the bulge in savings. As a result, there was

the unhealthy spectacle of the country’s current account getting into a

situation of surplus, that is, the counterpart of the negative capital

inflow. As shown in Table 2, the three year period 2001-02 to 2003-04

experienced negative capital inflows ranging from (-) 0.7% to (-) 2.2% of

GDP. That is, a saving-scarce economy like that of India experienced a

situation of net capital outflow. The reasons were not far to seek. The

root reason was the rapid bulge in capital inflows which contributed to

the phenomenal increases in the country’s foreign exchange reserves (Table

3). The bulge began precisely in 2002-03 which is associated with a number

of positive developments in the country’s macroeconomy thereafter

including the vast increases in domestic saving and investment. The

foreign exchange reserves, which had increased by $11.83 billion (Rs

66,831 crore) during 2001-02, expanded more rapidly thereafter by US

$21.99 billion (Rs 97,432 crore) in 2002-03 and 36.86 billion (Rs 128,659

crore) in 2003-04. Such sudden increases in foreign reserves could not be

absorbed by expanding investment in the economy contemporaneously and

hence these were current account surpluses or negative net capital inflows

for three years until 2003-04. But, by then, the country’s domestic

investment rate had begun to improve rather rapidly, though not

commensurate with the capital inflows or with the increases in the

domestic saving rates. The gross capital formation (GCF) rate jumped from

22.8% of GDP in 2001-02 to 25.2% in 2002-03 and further to 27.6% in

2003-04. But, after 2003-04, the investment rates have overtaken the

savings rates, thus absorbing the foreign capital inflow albeit

partly to finance current account deficits and increased investment. Thus,

the GFC rate has steadily risen to as high a figure as 39.1% in 2007-08.

|

Table 3: Foreign Exchange Reserves and their Annual Increases |

||||

|

Outstandings at End-March |

Annual Increase |

|||

|

A. Total Reserves |

||||

|

Year/ Year-End |

US $ million |

Rs crore |

US $ million |

Rs crore |

|

2008-09 |

251,985 |

1,283,865 |

-57,738 |

+ 45,900 |

|

2007-08 |

309,723 |

1,237,965 |

+ 110,544 |

+ 369,743 |

|

2006-07 |

199,179 |

868,222 |

+ 47,557 |

+ 191,835 |

|

2005-06 |

151,622 |

676,387 |

+ 10,108 |

+ 57,271 |

|

2004-05 |

141,514 |

619,116 |

+ 28,555 |

+ 128,987 |

|

2003-04 |

112,959 |

490,129 |

+ 36,859 |

+ 128,659 |

|

2002-03 |

76,100 |

361,470 |

+ 21,994 |

+ 97,434 |

|

2001-02 |

54,106 |

264,036 |

+ 11,825 |

+ 66,832 |

|

2000-01 |

42,281 |

197,204 |

+ 4,245 |

+ 31,291 |

|

B. Foreign Currency Assets |

||||

|

Year/ Year-End |

US $ million |

Rs crore |

US $ million |

Rs crore |

|

2008-09 |

241,426 |

1,230,066 |

-57,804 |

+ 34,043 |

|

2007-08 |

299,230 |

1,196,023 |

+ 107,306 |

+ 359,426 |

|

2006-07 |

191,924 |

836,597 |

+ 46,816 |

+ 189,270 |

|

2005-06 |

145,108 |

647,327 |

+ 9,537 |

+ 54,206 |

|

2004-05 |

135,571 |

593,121 |

+ 28,123 |

+ 126,906 |

|

2003-04 |

107,448 |

466,215 |

+ 35,558 |

+ 124,739 |

|

2002-03 |

71,890 |

341,476 |

+ 20,841 |

+ 92,358 |

|

2001-02 |

51,049 |

249,118 |

+ 11,495 |

+ 64,636 |

|

2000-01 |

39,554 |

184,482 |

+ 4,496 |

+ 31,558 |

|

Source: RBI, Bulletin (May 2009), Handbook of Statistics 2007-08 |

||||

Factors Influencing Jumps in Savings and Investments

As brought out above, the improvements in savings and investments after 2002-03 have been rapid and phenomenal; they have reached the levels attained in the south-east Asian economies including China, which have been high-growth epicentres in the world economy. These are a number of national and global developments since then which have contributed to the buoyant saving and investment scenario in the Indian economy.

Sizeable Capital inflows

|

Table 4: Foreign Investment Flows |

|||

|

(US $ million) |

|||

|

|

Direct Investment |

Portfolio Investment |

Total |

|

1 |

2 |

3 |

(2+3) |

|

2000-01 |

4029 |

2760 |

6789 |

|

2001-02 |

6130 |

2021 |

8151 |

|

2002-03 |

5035 |

979 |

6014 |

|

2003-04 |

4322 |

11377 |

15699 |

|

2004-05 |

6051 |

9315 |

15366 |

|

2005-06 |

8961 |

12492 |

21453 |

|

2006-07 |

22826 |

7003 |

29829 |

|

2007-08 (P) |

34362 |

29395 |

63757 |

|

2008-09 (Apr-Feb) |

31657 |

-12966 |

18691 |

|

Source: RBI, Bulletin (April 2009) |

|||

First, as a result of the continuous high growth performance of the world economy, particularly in the USA and other developed economies, there arose huge capital surpluses seeking investment in the emerging markets, and as a result of the series of the reforms measures, the Indian economy became an attractive destination for foreign capital inflows. The bulk of these in the form of portfolio inflows, began to see quantum jumps in 2003-04 as shown in Table 4. Such inflows grew from US $10 billion in 2002-03 to US $ 11.38 billion in 2003-04 and remained high thereafter. This has been associated with the high tempo of capital market and financial market activities in the Indian economy since then.

As indicated earlier, in fact the foreign exchange reserves had begun to expand in 2002-0 as a result of sizeable improvements in the country’s services export receipts and also in private remittances.

|

Table 5: Financial and Physical Savings of Household Sector (As percentage of GDP) |

|||||

|

Year |

Gross Financial Savings |

Financial Liabilities |

Net Financial Savings(2-3) |

Physical Saving |

Total Household Saving(4+5) |

|

1 |

2 |

3 |

4 |

5 |

6 |

|

1998-99 |

11.8 |

1.5 |

10.3 |

8.5 |

18.8 |

|

1999-00 |

12.1 |

1.8 |

10.3 |

10.5 |

20.8 |

|

2000-01 |

11.8 |

1.5 |

10.3 |

11.4 |

21.7 |

|

2001-02 |

13.0 |

2.3 |

10.7 |

11.3 |

22.0 |

|

2002-03 |

13.1 |

2.5 |

10.6 |

12.6 |

23.2 |

|

2003-04 |

13.7 |

2.5 |

11.2 |

12.7 |

23.9 |

|

2004-05P |

13.8 |

3.8 |

10.0 |

12.7 |

22.7 |

|

2005-06P |

16.7 |

5.1 |

11.6 |

12.4 |

24.0 |

|

2006-07P |

18.5 |

6.8 |

11.7 |

12.4 |

24.1 |

|

2007-08# |

15.6 |

4.4 |

11.2 |

12.6 |

23.8 |

|

P : Provisional; # : Preliminary |

|||||

|

Source: CSO press note dated 30th January 2009: RBI(2008) , Annual Report 2007-08 |

|||||

All of the above factors contributing to the growth of foreign currency assets and consequently to the expansion of financial liquidity in the system, have helped to improve household financial saving shown in Table 5, gross financial savings of households as percentage of GDP have made a leap from 11.8% in 2000-01 to 13.0% in the next two years and reached the peak of 18.5% in 2006-07. Alongside, there have also been some improvements in the household physical assets formation.

|

Table 6: Annual Sectoral Growth Rates in GDP at 1999-2000 Prices |

||||

|

(Growth Rate in Per Cent Per Annum) |

||||

|

Year |

Industry |

|||

|

1 |

2 |

3 |

4 |

|

|

Agriculture, Forestry and Fishing |

Industry |

Services |

GDP at Factor Cost |

|

|

2000-01 |

-0.2 |

6.4 |

5.7 |

4.4 |

|

2001-2002 |

6.3 |

2.7 |

7.2 |

5.8 |

|

2002-2003 |

-7.2 |

7.1 |

7.5 |

3.8 |

|

2003-2004 |

10 |

7.4 |

8.5 |

8.5 |

|

2004-2005 |

0 |

10.3 |

9.1 |

7.5 |

|

2005-2006 |

5.8 |

10.2 |

10.6 |

9.5 |

|

2006-2007@ |

4 |

11 |

11.2 |

9.7 |

|

2007-2008* |

4.9 |

8.1 |

10.9 |

9 |

|

@ Provisional Estimates * Quick Estimates |

||||

|

Source: Central Statistical Organisation (CSO) (2009): Quick Estimates Of National Income Consumption Expenditure, Savings And Capital Formation, 2007-08. |

||||

The above explanation provided for the increases in household saving may be considered as static balance sheet explanation. In fact, there is the dynamic economic process found in the acceleration of the rates of economic growth – and growth in household incomes that should provide a more solid basis for the recent expansion in household savings (Table 6).

Increases in Savings of Public and Private Corporate Sectors

It must be admitted that in relative terms, the improvements in household saving is not as large as in the case of public sector and private corporate sector. However, the same virtual causation between growth and savings is also applicable to the savings of the public sector and the private corporate sector. As shown in Table 7, the increases in savings as indicated above in respect of the household sector, have been found to be more true in the cases of the above two organised sectors. The public sector saving has improved from (-) 0.6. % of GDP in 2002-03 to .4.5.% in 2007-08 and the private corporate sector saving likewise has risen from .4.0% to .8.8.% during the same period. The general buoyant economic environment has made it possible for these sectors to produce high levels of savings (and investment) in the recent period.

|

Table 7: Sector-wise Domestic Savings (At Current Prices) |

||||||

|

(As Percentage to GDP at Current Market Prices) |

||||||

|

Year |

Household Sector |

Private Corporate Sector |

Public Sector |

Gross Domestic Savings (4+5+6) |

||

|

Financial Savings |

Physical |

Total (2+3) |

||||

|

1 |

2 |

3 |

4 |

5 |

6 |

7 |

|

New Series (Base: 1999-2000) |

||||||

|

1999-2000 |

10.6 |

10.5 |

21.1 |

4.5 |

-0.8 |

24.8 |

|

2000-2001 |

10.2 |

11.4 |

21.6 |

3.9 |

-1.8 |

23.7 |

|

2001-2002 |

10.9 |

11.3 |

22.1 |

3.4 |

-2 |

23.5 |

|

2002-2003 |

10.3 |

12.6 |

22.9 |

4 |

-0.6 |

26.3 |

|

2003-2004 |

11.4 |

12.7 |

24.1 |

4.6 |

1.1 |

29.8 |

|

2004-2005 |

10.1 |

12.7 |

22.8 |

6.7 |

2.2 |

31.7 |

|

2005-2006 |

11.7 |

12.4 |

24.1 |

7.7 |

2.4 |

34.2 |

|

2006-2007@ |

11.7 |

12.4 |

24.1 |

8.3 |

3.3 |

35.7 |

|

2007-2008* |

11.7 |

12.6 |

24.3 |

8.8 |

4.5 |

37.7 |

|

@ Provisional Estimates * Quick Estimates |

||||||

|

Source: As in Table 1.1 |

||||||

However, there are also some components of public policies which have created a conducive environment for the public sector and the private corporate sector to generate higher levels of savings.

Fiscal Discipline and Reductions in Revenue Deficits of the Government Sector

|

Table 8: Gross Fiscal Deficit & Revenue Deficit of Centre, States and Combined |

||||||

|

(As % to GDP) |

||||||

|

Gross Fiscal Deficit |

Revenue Deficit |

|||||

|

Centre |

States |

Combined |

Centre |

States |

Combined |

|

|

2001-02 |

6.1 |

4.2 |

9.9 |

4.4 |

2.6 |

6.9 |

|

2002-03 |

5.9 |

4.1 |

9.5 |

4.4 |

2.2 |

6.6 |

|

2003-04 |

4.5 |

4.4 |

8.4 |

3.6 |

2.2 |

5.8 |

|

2004-05 |

4.0 |

3.5 |

7.5 |

2.5 |

1.2 |

3.7 |

|

2005-06 |

4.1 |

2.5 |

6.7 |

2.6 |

-0.6 |

2.7 |

|

2006-07 |

3.5 |

1.9 |

5.6 |

1.9 |

-0.3 |

1.3 |

|

2007-08 |

2.7 |

2.3 |

5.3 |

1.1 |

-0.5 |

0.9 |

|

2008-09 |

6.0 |

2.1 |

4.4 |

-0.5 |

||

|

2009-10 |

5.5 |

4.0 |

||||

|

Source: GOI Budget Documents and RBI Annual Reports |

||||||

The public sector savings comprise retained earnings of departmental and non-departmental enterprises as well as saving of the general government administration. As in the case of the private corporate sector, the commercial enterprises of the government - departmental and non-departmental –have derived the benefits of higher activities and larger savings. Within the public sector, the segment that has achieved substantial improvement in savings relates to the savings of the public administration. This is almost entirely due to the implementation of the Fiscal Responsibility and Budget Management (FRBM) Act and the rules framed there under. The results of this fiscal discipline, germane to the estimation of savings, are reflected in rapid decline in the combined revenue deficit of the central and state governments. As shown in Table 9, there has occurred a sharp decline in the combined revenue deficit from 6.9% in 2001-02 to just 0.9% in 2007-08.

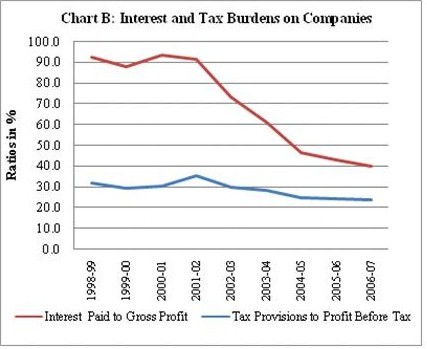

Higher Profits Lower Taxes and Reduced Interest Burden of the Corporate Sector

The private corporate

sector has derived allround benefits of economic, fiscal and monetary

reforms. As shown in the results of the RBI studies on company finances

(Table 9), gross profits to sales ratio of the sample public limited

companies has shown a steady improvement since 2001-02; from about 10%, it

has touched 14.2% in 2006-07. But that is not all; the corporate sector

has derived historically the highest level of benefits from two key

sources: reduced interest burden; and lower incidence of corporate

taxation. These crucial public policies, put in place for encouraging

increased investment and expansion of productive capacity, are reflected

in-huge benefit derived the corporate sector at first remove in the form

of significant declines in (i) the ratio of tax provisions to profits

before tax; and (ii) the proportion of interest paid to gross profit. The

former ratio has come down from about 37% in 2001-02 to 24% in 2006-07 and

the latter has dropped from 58% to 16% during the same period. Obviously,

the benefits of these liberal public policies for the corporate sector

have indeed been very large and they would have directly contributed to

the increases in corporate sector savings.

As shown in the results of the RBI studies on company finances

(Table 9), gross profits to sales ratio of the sample public limited

companies has shown a steady improvement since 2001-02; from about 10%, it

has touched 14.2% in 2006-07. But that is not all; the corporate sector

has derived historically the highest level of benefits from two key

sources: reduced interest burden; and lower incidence of corporate

taxation. These crucial public policies, put in place for encouraging

increased investment and expansion of productive capacity, are reflected

in-huge benefit derived the corporate sector at first remove in the form

of significant declines in (i) the ratio of tax provisions to profits

before tax; and (ii) the proportion of interest paid to gross profit. The

former ratio has come down from about 37% in 2001-02 to 24% in 2006-07 and

the latter has dropped from 58% to 16% during the same period. Obviously,

the benefits of these liberal public policies for the corporate sector

have indeed been very large and they would have directly contributed to

the increases in corporate sector savings.

|

Table 9: Finances of Non-Government Non-Financial Public Limited Companies (Selected Ratios in Per Cent) |

|||||

|

Year |

Number of Companies |

Selected Ratios in Per Cent |

|||

|

Gross Profits To Sales |

Tax Provisions to Profit Before Tax |

Interest Paid to Gross Profit |

Remu- neration to Sales |

||

|

(1) |

(2) |

(3) |

(4) |

(5) |

(6) |

|

2006-07 |

3016 |

14.2 |

24.0 |

16.1 |

7.4 |

|

2005-06 |

|

12.4 |

24.6 |

18.6 |

7.3 |

|

2004-05 |

|

12.2 |

24.8 |

22.0 |

7.2 |

|

2005-06 |

2730 |

12.2 |

25.4 |

18.1 |

7.1 |

|

2004-05 |

|

11.4 |

25.9 |

23.0 |

7.0 |

|

2003-04 |

|

10.9 |

28.7 |

32.4 |

7.8 |

|

2004-05 |

2214 |

11.9 |

25.7 |

21.8 |

7.5 |

|

2003-04 |

|

11.1 |

28.1 |

30.7 |

8.0 |

|

2002-03 |

|

10.3 |

29.9 |

43.6 |

8.1 |

|

2003-04 |

2201 |

11.4 |

27.9 |

30.1 |

7.9 |

|

2002-03 |

|

10.4 |

30.5 |

43.1 |

8.0 |

|

2001-02 |

|

9.8 |

35.5 |

56.0 |

7.9 |

|

2002-03 |

2031 |

10.3 |

31.3 |

47.9 |

8.0 |

|

2001-02 |

|

10.2 |

36.7 |

58.3 |

8.0 |

|

2000-01 |

|

9.8 |

30.4 |

63.2 |

7.3 |

|

2001-02 |

2024 |

9.6 |

35.6 |

59.0 |

7.8 |

|

2000-01 |

|

9.2 |

31.1 |

63.2 |

7.2 |

|

1999-00 |

|

10.1 |

29.4 |

58.7 |

7.2 |

|

2000-01 |

1927 |

10.1 |

32.3 |

60.0 |

8.2 |

|

1999-00 |

|

10.5 |

33.2 |

59.3 |

8.2 |

|

1998-99 |

|

10.7 |

32.0 |

60.6 |

8.5 |

|

Source: RBI (2008) : Finances of Public Limited Companies, 2006-07, Reserve Bank of India Bulletin, March and respective earlier issues. |

|||||

Highlights of Current Economic Scene

Agriculture

The central government would be allowing private traders to exports 2 million metric tonnes of wheat from May 15 2009. Private companies are requested to purchase wheat from the market for overseas sales, as the government has decided that it won’t be using its reserves for exports. Apart from wheat, exports of wheat products like sooji, maida and atta would also be allowed to be exported.

Wheat procurement by the central government, so far, has increased by nearly 20% in the 2009-10 (April-March) marketing season at 212.54 lakh tonnes as against 177.52 lakh tonnes during the same period last year. The government has targeted to procure 244 lakh tonnes of wheat in the current season. To achieve the target it started purchasing the grain in Madhya Pradesh, Rajasthan and Gujarat on 18 March, while in remaining states it started on 01 April. Of the 212.54 lakh tonnes of wheat, FCI purchased 38.81 lakh tonnes, while co-operatives procured 57.66 lakh tonnes. Procurement in Punjab stood at 104.21 lakh tonnes as on 08 May, compared to 93.34 lakh tonnes in the same period last year. While procurement in Haryana was reported to be at 36,493 tonnes, in Uttar Pradesh it was 1.59 lakh tonnes and Madhya Pradesh 57,258 tonnes, respectively.

The Centre had procured over three lakh tonnes of bajra from Haryana at a rate of Rs 812 per quintal lower than the minimum support price (MSP) of which it would be disposing 11,000 tonnes. It has also procured about 7,000 tonnes of bajra from Madhya Pradesh, Karnataka and Maharashtra in 2008 kharif season, as market prices were lower than its MSP at that time. Currently, bajra prices at the regulated market yard (mandi) are hovering in the range of Rs 600-1,190 per quintal depending on the quality and variety.

Coverage under gaur in Rajasthan is likely to fall by 9.74% in 2009-10 crop year at 2.5 million hectares from 2.77 million hectares of last year. Most of the farmers cultivating gaur are expected to opt for cotton and cereals, as they are likely to fetch better prices. Gaur acreage in the state increased in 2007-08, as price of the commodity showed a drastic rise. Rajasthan, which accounts for about 70% of the country's guar output, covered an average area of 2 million hectares under this crop during 2002-03 to 2006-07.

As per government sources, state-run trading firms have contracted to import an additional 30,400 tonnes of white sugar from Brazil and Thailand, taking purchases to 50,400 tonnes this year. State Trading Corporation of India Ltd. has ordered 25,000 tonnes from Thailand, MMTC Ltd. has contracted 5,400 tonnes from Brazil, while PEC had earlier decided to import 15,000 tonnes of white sugar from Thailand and 5,000 tonnes from Brazil. Sugar mills have requested the importing agencies to buy white sugar on their behalf.

According to the Textiles Ministry, exporters, so far, have shipped 1.2 million bales after the government made registration of export contracts mandatory to curb domestic prices in the month of July 2008. Domestic cotton suppliers sought permission from the central government to export 2.4 million bales in the nine month period that ended in the month of April. Cotton output may drop by 8% to 29 million bales during the year ending 30 September 2009 as against the previous year and shipments this year would drop to 5 million bales from 8.5 million bales of the last year. Traders have also registered to export 67,950 bales of cotton waste between August and April. In total 40,427 bales have so far been shipped from the country. Cotton Corporation of India (CCI) has reiterated that market arrivals would drop to 27 million bales as of 02 May 2009 down from 29.7 million bales a year ago.

According to latest data compiled by the Solvent Extractors' Association (SEA), oilmeal exports dropped sharply by 64% during April 2009 to 2.32 lakh tonnes as compared to 6.47 lakh tonnes in April 2008, mainly on reduced demand for compound feeds globally. Meat production declined in Europe, the US and the other countries. Poultry production has slowed down notably in Brazil and marginally in India. Several Asian countries suffered from a crisis in the livestock industry, which contributed to lower consumption of soyameal and other oilmeals reflected in lower exports.

Exports of castor oil has registered a significant growth of 74% to 3.08 lakh tonnes during the fiscal year 2008-09 from 1.76 lakh tonnes during the same period a year ago. This resulted due to good purchase of the product by China. The country has so far exported about 75,000 tonnes of castor oil till April during the current calendar year, as fresh arrivals of new crop has started to enter into the market since January. It is predicted that daily arrivals in the market has reached to one-lakh bags (each of 75 kgs).

As per the report by US Department of Agriculture (USDA), coffee exports from India are expected to jump by 21% to around 230,000 tonnes in the financial year 2010 season starting from October due to expected increase in production. However, during October-April 2009, coffee exports are expected to decline to around 1, 90, 000 tonnes because of reduced exportable surplus and high domestic prices vis-à-vis lower global prices. Exports would be lagging behind by 25,000 tonnes as compared to the corresponding period of the previous year.

According to the government's trade promotion body ‘Agricultural and Processed Food Products Exports Development Authority’ (APEDA), mango exports to the US have stood at 31.7 tonnes in April this year, compared to around 20 tonnes in the corresponding period last year. During 2008 mango season starting from April, exports from the country stood at 143 tonnes of mangoes to the US valued at around Rs 2 crore. According to trade estimates, the output is expected to decline by 30% to 8 million tonnes in 2009 season, compared with 11.9 million tonnes in a year-ago period.

Industry

The General Index (IIP) stands at 297.9, which is 2.3% lower as compared to the level in the month of March 2008. The cumulative growth for the period April-March 2008-09 stands at 2.4% over the corresponding period of the previous year.

The annual growth of thee Indices of Industrial Production for the Mining, Manufacturing and Electricity sectors for the month of March 2009 at 0.4%, (-)3.3% and 6.3% as compared to March 2008. The cumulative growth during 2008-09 over the corresponding period of 2007-08 in the three sectors have been 2.3%, 2.3% and 2.8% respectively, which moved the overall growth in the General Index to 2.4%.

In terms of industries, as many as five (5) out of the seventeen (17) industry groups (as per 2-digit NIC-1987) have shown positive growth during the month 2009 as compared to the corresponding month of the previous year. The industry group ‘Beverage etc’ have shown the highest growth of 15.1%, followed by 8.3% in ‘basic chemicals ’ and 6.6% in ‘Rubber and plastic products’. On the other hand, the industry group ‘Food Products’ have shown a negative growth of 35.8% followed by 25.1% in ‘Wood and Wood Products; Furniture and Fixtures‘ and 18.1% in ‘Leather and Leather Products’.

As per Use-based classification, the Sectoral growth rates in March 2009 over 2008 are 1.4% in Basic goods, (-)8.2% in Capital goods and (-) 4.4% in Intermediate goods. The Consumer durables and Consumer non-durables have recorded growth of 8.3% and (-) 3.4% respectively, with the overall growth in Consumer goods being negative at 0.8%..

Infrastructure

The Index of Six core industries having a combined weight of 26.7 per cent in the Index of Industrial Production (IIP) with base 1993-94 stood at 270.3(provisional) in March 2009 and registered a growth of 2.9% (provisional) compared to a growth of 2.9% in March 2008. During April-March 2008-09, six core industries registered a growth of 2.7% (provisional) as against 5.9% during the corresponding period of the previous year.

Crude Oil production registered a decline of (–)2.3% in March 2009 compared to a lower fall of (-)0.3% in March 2008. The Crude Oil production registered a growth of (-) 1.8 during April-March 2008-09 compared to 0.4% during the same period of 2007-08.

Petroleum refinery production registered a growth of 3.3% (provisional) in March 2009 compared to growth of 0.1% in March 2008. The Petroleum refinery production registered a growth of 3.0%during April-March 2008-09 compared to 6.5% during the same period of 2007-08.

Coal production registered a growth of 5.2% in March 2009 compared to growth rate of 9.3% in March 2008. Coal production grew by 8.1% during April-March 2008-09 compared to an increase of 6.0% during the same period of 2007-08.

Electricity generation registered a growth of 5.9% (provisional) in March 2009 compared to a growth rate of 3.6% in March 2008. Electricity generation grew by 2.7% during April-March 2008-09 compared to 6.3% during the same period of 2007-08.

Cement production registered a growth of 10.1% in March 2009 compared to 9.3% in March 2008. Cement Production grew by 7.5% during April-March 2008-09 compared to an increase of 8.1% during the same period of 2007-08.

Finished (carbon) Steel production (weight of 5.13% in the IIP) registered a growth of (-)2.6%in March 2009 compared to (-)0.9% in March 2008. Finished (carbon) Steel production grew by 0.4% during April-March 2008-09 compared to an increase of 6.2% during the same period of 2007-08.

Inflation

The official Wholesale Price Index for 'All Commodities' (Base: 1993-94 = 100) for the week ended 25th April, 2009 rose by 0.2 percent. The annual rate of inflation, calculated on point to point basis, stood at 0.70% for the week ended 25/04/2009 as compared to 0.57% for the previous week and 8.27% during the corresponding week of the previous year.

The index for major group Primary articles rose by 0.2% due to higher prices of tea, bajra,,arhar,milk, wheat, condiments and spices,jowar, castor seed, soyabean, and linseed.

The index for fuel, power ,light and lubricants remained stable at 323.0 for the week.

The index for manufactured products gone-up by 0.3 percent to 202.2 from 201.6 for the previous week. The index for 'Food Products' group rose by 1.3%. due to higher prices of rice bran oil , sugar, khandsari .ghee and gingelly oil.

The index for 'Chemicals & Chemical Products' group rose by 0.3% due to rise in prices of vitamin tablets, syrup, purified terephthalic acid and acid all kinds.

The index for 'Basic Metals Alloys & Metal Products' group fell by 0.1% due to fall in prices of zinc, zinc ingots and lead ingots.

The final wholesale price index for ‘All Commodities’ (Base:1993-94=100) revised upwards from 227.7 to 227.8 for the week 28 February 2009. and hence the annual rate of inflation based on final index, calculated on point to point basis, stood at 2.47 percent as compared to 2.43 percent.

Financial Market Developments

Capital Markets

Primary Market

Primary market remaining dull during the week as there was no issues entering the Capital market to mobilize funds.

Secondary Market

Momentum buying lifted the market for the eighth consecutive week on expectations of a recovery in the Indian and global economy. A recent reduction in interest rates also powered the market higher. A forecast by the Meteorological Department of a near normal monsoon as well as better-than-expected fourth quarter earnings announced by some key corporates also provided fillip to the market sentiment. The BSE Sensex registered a weekly gain of 74.2 points or 0.7% to 11,403. As against the gains seen in large caps, the BSE mid and small cap indices fell by 2.14% and 3.1% respectively last week. But the NSE Nifty fell 6.8 points or 0.2% to 3474 during the week. The BSE Mid-Cap index fell 2.4% to 3,5134 and the BSE Small-Cap index fell 3.1% to 3941 during the week. The Defty was down 0.74% as the rupee lost ground and dipped below the $50 mark.

Most of the sectoral indices of BSE recorded positive returns over the week except Consumer Durable, Realty and FMCG index. Among the gainers IT recorded 9.9% growth followed by Bankex, TECk and Auto with 7.8%, 6.4% and 6.3%, respectively. Better than expected numbers from Teck firms and a weak rupee pushed up the IT indices. TECk index rose due to good results from Bharti. The Bankex rose on hopes that lower rates would boost asset growth.

Foreign institutional investors (FIIs) made heavy purchases. FII inflow in April 2009 totaled Rs 7,039.90 crore, and the inflow in calendar year 2009 totaled Rs 368.10 crore (till 28 April 2009). Mutual funds sold stocks worth Rs 396 crore during the week.

The Securities and Exchange Board of India (SEBI) is in talks with the Reserve Bank of India (RBI) to introduce foreign currency options on the exchanges. As per media sources a seven-member standing committee, with representatives from both SEBI and RBI, is working on the modalities to bring in foreign currency options by October 2009. The move assumes a huge significance in view of the heavy losses that companies had incurred in overseas cross-currency options deals last year.

The SEBI is in talks with the RBI to consider a proposal to permit dollar settlements for FIIs in India. The move would mean a tectonic shift in the way FIIs invest in Indian markets. Dollar settlements would not only mitigate risks of currency fluctuations for FIIs, but also help in improving the volume and liquidity of the derivatives market. At present, settlements in India are done in rupee denominations. As a result, a number of FIIs, who intend to trade in Nifty futures, take the Singapore route where CNX Nifty index futures are traded on SGX. If dollar settlement is allowed in India, many participants, who want to take exposure to Indian markets through index buying, will be able to participate freely. This, in turn, will give stability to Indian markets as there will be buying of underlying stocks by the sellers of these contracts to FIIs. Sources close to the development said that it was a consultative process between RBI and Sebi and that it was difficult to fix a time frame as to when guidelines on this would be issued. RBI has formed a committee to discuss the issue.

Derivatives

The three-day trading week saw Nifty future end on a flat note as Wednesday’s smart recovery ensured that previous two sessions losses were recouped. The Nifty closed out a truncated week at 3,473.95 points for a small nominal loss. Despite truncation due to voting in Mumbai, the April settlement saw a very high carryover into May. The Nifty April future closed about 3,474 points against its previous week’s closing of 3,482. April saw massive increases in trading volumes along with continuous price rise. Nifty May future closed a tad higher at about 3,483 points. The series also saw a slightly higher rollover of 74%. The market-wide rollover, however, was about 70%, way below its performance in the earlier expiry. Quite a few stock futures did not active rollover like last month. Expulsion of 50 stocks from the F&O list and the uncertainty related to election outcomes could be attributed to the poor show. Stock futures in telecom, auto and IT sectors however reported strong rollovers.

FIIs have remained net buyers who poured over Rs 7,000 crore into equities in April, domestic institutions have been heavy net sellers in the past fortnight. The FIIs continue to hold around 37% of all open interest. The CNXIT sustained the market last week when it produced strong positive returns on the back of a rupee that dropped below 50. The May Nifty put-call ratio (PCR) in terms of open interest ratio is down to around 1.1

Volatility index, which measures the immediate expected volatility, weakened slightly during the week. It ended at 46.63 as compared with its previous week’s close of 47.78. The fall however was mainly due to the expiry of April contracts, as some traders did not roll over their put positions. The cumulative FII positions as a percentage of the total gross market position on the derivative segment as on 29 April jumped to 43.29%. They resorted to heavy selling, particularly in index futures. They now hold index futures worth Rs 11,597.73 crore (Rs 13,286.71 crore) and stock futures Rs 14,534.88 crore (Rs 18,447.89 crore). They reduced index options holding significantly to Rs 22,771.88 crore (Rs 34,658.94 crore).

Government Securities Market

Primary Market

RBI auctioned 91-day TBs and 364-day TBs on 6 May 2009 for the notified amount of Rs 8,000 crore and Rs 1,000 crore, respectively. The cut-off yield for the 91-day TBs and 364-day TBs were set at 3.15% and 3.50%, respectively.

The State Government of West Bengal auctioned 10-year paper maturing in 2019 for the notified amounts of Rs 2,500.00 crore on 6 May 2009.

Secondary Market

Inter-bank call rates moved in the range of 3.23-3.27% during the week. Bonds remained steady as traders booked profits though financial markets continued to be dogged by the liquidity overhang. At the weekend liquidity adjustment facility auctions the recourse to the reverse repo window amounted to Rs 89,350 crore.

Bond Market

During the week under review, 1 FIs/banks, 1 NBFC, 1 corporate and 1 central undertaking tapped the bond market to mobilize an amount of Rs 1,275 crore, respectively.

|

Profile of Major Commercial Bond Issues for the Week Ending 01 May 2009 |

||||

|

Sr |

Issuing Company / Rating |

Nature of Instrument |

Coupon in % per annum and tenor |

Amount in Rs. crore |

|

No |

||||

|

|

FIs / Banks |

|

|

|

|

1 |

ICICI Home Finance

Ltd |

NCD |

8.25% for 5 years. |

75 |

|

|

NBFCs |

|

|

|

|

1 |

Power Finance Corp

Ltd |

Bonds |

6.90% and 7.50% for 3 years and 5 years, respectively. |

300 |

|

|

Corporates |

|

|

|

|

1 |

Edelweiss Capital

Ltd |

NCD |

9.25% for 2 years. |

200 |

|

|

Central Undertakings |

|

|

|

|

1 |

NTPC Ltd |

Bonds |

7.89% for 10 years. |

700 |

|

|

Total |

1275 |

||

|

|

Source: Various Media Sources |

|||

On 28 April, Anil Ambani group firm Reliance Communications said that it has bought back 247 zero coupon foreign currency convertible bonds (FCCBs) worth Rs 125 crore (USD 24.7 million) from the international markets. In a filing to the BSE, the company declared that the repurchased FCCB's are expected to be extinguished shortly. Last year, the RBI had allowed the corporate houses to buy back FCCBs from the foreign markets if they are trading at a discount of 25% from their book value.

Indian companies are borrowing money overseas to buy back the FCCBs that were issued by them and are now selling at a steep discount. Details on foreign loans, termed external commercial borrowings (ECBs) by the regulator, reveal that the major borrowers in March 2009 were telecom company Aircel, which received permission to raise half a billion dollars, and flag carrier National Aviation Company, which got a clearance for $136 million to fund their expansion plans. The data also shows that six corporates were given the nod to raise funds abroad to repurchase FCCBs. Following buybacks, the prices of Indian FCCBs have improved in the secondary market. Last week, the RBI further liberalised the norms for repurchase of FCCBs by allowing corporates to buy back FCCBs worth $100 million. The central bank has also extended the relaxed guidelines for international borrowing up to December 2009. The numbers show that despite a relaxation in overseas borrowing norms, the trend of lower borrowing continued till the end of the fiscal. In March, the central bank had approved borrowings worth only $1.1 billion; this is around a fourth of the $4.4 billion raised in March 2008. In FY08, the funds raised through ECBs amounted to 20.5 billion. The total ECB sanctioned for the year, including FCCB, was $19 billion, compared to $22.6 billion sanctioned for the previous year. In the second half of FY09, the RBI had substantially liberalised the overseas borrowing norms.

Foreign Exchange Market

The rupee fell by around 25 paise against the dollar on May 11, 2009, after losing most of the intra-day gains. The rupee opened with a positive gap at 49.10 and strengthened to touch an intra-day high of 49.05. It weakened to close at 49.52, against the previous close of 49.28. The higher opening was on account of euro’s rally against the greenback in the previous trading session and the positive global equity markets, said a dealer with a private bank. However, it lost most of the gains tracking the negative domestic equity indices, added the dealer. In the overseas markets, the dollar gained a bit against the euro and the pound but was flat against the yen. In the forward premia market, the six-month premium closed at 2.75 per cent and the one-year closed at 2.26 per cent.

Commodities Futures derivatives

Commodity market regulator Forward Markets Commission (FMC) has directed exchanges to relook at the spot-futures disconnect in potato as the data supplied by Multi Commodity Exchange of India (MCX) and National Commodity & Derivatives Exchange (NCDEX) on the commodity’s high futures prices have failed to satisfy the regulator on the market dichotomy. The exchanges are likely to revert to FMC by the weekend. A few weeks ago, the regulator asked multi commodity exchanges - NCDEX, MCX and Ahmedabad-based NMCE - to justify runaway prices in sugar, rubber, turmeric and potato futures.

The country’s top two commodity exchanges, MCX and NCDEX, have imposed special margin on sugar futures in an attempt to curb volatility in prices of the sweetener at the futures market. The measure has been taken on the direction of the commodity market regulator FMC. The FMC was recently asked by the committee of secretaries (COS) to watch the movement in sugar prices in the futures market and take necessary steps to curb excessive speculation. According to an NCDEX circular, the exchange has imposed 5% special margin on long positions of all running contracts of sugar except for contract expiring in August 2009. After the imposition the total special margin levied on sugar will be 10% on the long side on all contracts except for August, which will remain at 15%. Similarly the MCX has fixed 10% special margin on both M and S grade of sugar traded on the exchange, the MCX circular said. Special margin is effective on both the exchanges from 4 May 2009.

Ahmedabad-based agri commodity bourse National Multi Commodity Exchange (NMCE) has seen a sudden spurt in average daily turnover (ADT) over the past two months. From Rs 220 crore in January, ADT shot up to Rs 839 crore in March’09 before moderating to Rs 542 crore in April. For an exchange that has seen ADT range between Rs 275 crore and Rs 400 crore in previous fiscals, this rise is stupendous. ADT for rival bourse NCDEX stood at around Rs 1,500 crore in March, according to an exchange official. While the rise may be attributed in part to reactivation of contracts such as sacking bags, coffee and kapas by NMCE in FY09 and to the launch of the evening session since September 2008, which resulted in increased participation in bullion and metals, traders relate it mainly to increased speculative activity in the final months of the fiscal. . The rise in speculative activity on NMCE can be determined by the high volume to open interest (OI) ratio. OI indicates rising market participation. A very high multiple (volume/OI) indicates a high level of speculative activity, or day trades.

After lying dormant for quite some time, futures trading in agri commodities at 22 commodity exchanges showed a sign of pick-up and the turnover of farm items shot up by 18.40% to Rs 36,400 crore in the first fortnight of the current fiscal, FMC has said. The exchanges had generated a business of Rs 30,744 crore in agricultural futures in the corresponding period last year, the commodity market regulator Forward Markets Commission (FMC) said in a release. Trade volume and investors' participation in the futures trading in farm commodities had witnessed a setback due to a ban on potato, chana, rubber and soya oil in 2008, which was lifted after six months. Agri futures, however, has shown improvement in the first fortnight of 2009-10 fiscal.

On 29 April Jeera futures on the NCDEX hit 2% upper circuit mainly on reports of lower supplies, uncertainty over crops in Syria and Turkey supported by reduced inflows in Unjha centre. NCDEX jeera May contracts were traded higher at Rs 12,165 on Wednesday over the previous day’s close of Rs 11,914 per quintal, up by 2.10% on reports of bad weather in the major producing regions. Report on the production front from Turkey, Syria and Iran is likely to have a short term impact on the prices.

Notwithstanding slowdown in gold sales even during the auspicious occasion of Akshaya Tritiya, small investors have been increasingly shifting their focus towards gold as an investment option during the last one year. The MCX which launched its first ever gold guinea futures contract a year back has already sold 44,125 guineas (8 gram each). More than 352 kg of gold has been purchase by small investors through buying of these guineas. Small retail investors have been specially showing interest in the product because of 'physical delivery' and quality certification from London Bullion Market," Ashok Mittal, vice-president, Karvy Comtrade, told FE. Investors have taken delivery of 715 gold guineas from Karvy during the April 2009. Another factors going in favour of gold guinea is that eight gram gold guinea are not only being physically delivered at home but also sold at around 15% less than the market price of gold coin sold by financial institutions and banks. The guinea prices have moved from Rs 9,661 per 8 gram on 8 May 2008 to Rs 11,370 for the April 2009 contract, a rise of more than 15%.

MCX received a major blow after the Central Electricity Regulatory Commission (CERC) ruled that it has jurisdiction to regulate the forward contracts in electricity. However, till its regulations and guidelines for electricity forward contracts come into effect MCX transactions in forward contracts in electricity will be governed by CERC’s existing orders. CERC issued order on a petition filed by NSE promoted Power Exchange India (PXI) with an appeal to restrain MCS and Indian Energy Exchange (IEX) from introducing, selling, marketing or otherwise dealing in any manner with electricity forward contracts. MCX had submitted that by virtue of the notification issued by the Centre only FMC had the jurisdiction to regulate the forward contracts in electricity through an association recognised under section 6 of the 1952 Act.

Buyers from the spot exchange, however, will have to pay Rs 200 for every turnover of Rs 1 lakh. NSEL, which was launched in October last, is awaiting licence from Tamil Nadu to commence spot trading in various agricultural products. It expects the licence in a month’s time after which different contracts will be offered in different places such as Salem, Madurai and Coimbatore.

Banking

Allahabad Bank has registered an increase of 55.8% in the net profit for the quarter ending March 31, 2009, driven by rise in its treasury income and net interest margin and a fall in cost of deposits. The net profit for 2008-09 has gone down by 21.2% owing to higher provisioning for investment depreciation and income tax.

Indian Overseas Bank (IOB) has reported a 10.3% growth in its net profit for the fiscal ended March 31, 2009 to Rs 1,326 crore as against Rs 1,202 crore during the previous fiscal. The total income increased by 28% to Rs 11,237 crore as compared to Rs 8,776 crore.

ICICI bank is planning to open 580 new branches this year. However, the bank will not hire any new staff for the newly-opened branches, as the bank would be “re-skilling and re-training” some people from the existing workforce of around 36,000 employees in accordance with the needs of the expanded branch network.

Bank of Baroda has announced reduction in interest rates on deposits by 25 basis points having tenure of over 181 days which will be effective from 11 May 2009.

HDFC, India’s largest home loan financing company, for the quarter ended March 31, 2009 has posted net profit of Rs 733 crore as against Rs 768 crore in the corresponding quarter in the previous year, registering a decline of 4.5%. HDFC’s Q4 profits in 2007-08 was higher owing to one-time gain of Rs 202 crore from the sale of its 26% stake in HDFC General Insurance to Munich Re. Excluding the one-time gain, the net profit for the fourth quarter (2008-09) would have been higher by 20%. Loan approvals of HDFC during 2008-09 were worth Rs 49,166 crore against Rs 42,520 crore in the previous year, registering a growth of 16%.

The country’s largest lender, State Bank of India (SBI) has recorded an impressive 45.6% increase in its net profit to Rs 2,742 crore in the fourth quarter of 2008-09 propelled by interest income and other income, from Rs 1,883 crore posted in the corresponding period last fiscal. During the financial year 2008-09 the net profit of the bank increased by 35.5% to Rs 9,121 crore as against Rs 6,729 crore in 2007-08.

Corporate

ACC cement’s production in the month of April 2009 increased to 1.84 million metric tonne against 1.80 million metric tonne during the same month last year, recording a growth of 2.2%.

L&T has entered in to a pact with Europe’s EADS (Defence & Security) for the development and manufacturing of high-end defence electronics products, mobile systems and solutions for both India and international market. The company will spend Rs 2000 crore in the defence related business over the next 3-5 years. L&T is looking forward to set up three separate companies to look after defence, aerospace, and nuclear power by 2012-13.

Bharati Shipyard Ltd (BSL) has acquired almost 15% stake of Great Offshore for Rs 174 crore. BSL has bought 55,33,786 equity shares of the Great Offshore at Rs 315 per share.

India’s largest power generator, NTPC to fund its ongoing capacity addition of 22,4300 Mw is raising capital in the domestic market. The company is planning to raise Rs 11,330 crore in 2009-10 of which NTPC will be borrowing Rs 8,500 crore loan from SBI at a floating rate of interest during 2009-10. The loan will be disbursed in tranches and will be utilised in 3-7 years and will be made available in tranches.

Tata Motors has garnered nearly Rs 2,500 crore from 2.03 lakh fully-paid orders for the Tata Nano, a week after the booking process for the car came to a close. As much as 70% of the 2.03 lakh bookings received were financed, while the remaining 30% of the applications booked in cash by paying virtually the full cost of the vehicle upfront. Around 4,000 cash bookings were made online. Tata Motors announced that the first 1- lakh allottees from among the applicants would be chosen through a computerised randon selection procedure, and allotment will made within 60 days of booking closure. The maximum numbers of bookings were received for the top-end model, accounting for half the overall applications. The Nano car is scheduled to hit the roads in July. However, the number of fully-paid bookings is far lower than the number of booking forms sold at various centres. Around 6.10 lakh forms were purchased from these bookings centres. The amount mobilized through Nana booking comes as a relief to the company, which posted a loss of Rs 263 crore in Q3 2008-09 as against a profit of Rs 499 crore a year earlier.

The country’s largest real estate firm, DLF may have to pay Rs 400 crore in additional tax following a special audit of its books for the assessment year 2005-06 by the income tax department.

Recently Religare Venture Capital Limited, a wholly owned subsidiary of Religare Enterprises, and private equity player Milestone Capital formed a 50:50 joint venture (JV). The newly formed JV is making its investment within a month by acquiring a majority stake in a mid-sized (150-bed) hospital in the country by investing Rs 50 crore.

External Sector

Exports during March 2009 at US$ 11516 million which was one-third lower than that in March 208, as a result during the fiscal year 2008-09 total exports at US$ 168704 million registered a growth of 3.4% over that of US $ 163132 million reported in the comparable period last year.

Imports during March were valued at US $ 15561 million, a decrease of 34.0 per cent over that of US$ 23574 million in March 2008 and the cumulative import at US$ 287759 million was 14.3% more than that of US $ 251654 during 2007-08.

Trade balance during March worked out to be $ 4045 as compared to $6320 in 2007-8. The cumulative trade balance for 2008-09 estimated at US $ 119055 million was 1.3 times to that of US $ 88522 million during 2007-08.

While oil imports during the current fiscal year gone up from US $ 93176 million to US $ 79715 million, that of non-oil imports accelerated by 13.2% to US $ 171940 million.

Information Technology

Adlabs Films, Reliance group company has announced its launch of a BPO business for the media domain. Spread over 90,000 sq ft, the BPO which has 300 employees is planning to increase its headcount to 1200 employees within a year and will comply with Motion Pictures Association of America (MPAA) standards. The BPO will be providing a comprehensive one-point solution for the transition from analog to digital and from physical media to digital data. It will be one of the world’s largest comprehensive digital restoration and content processing services facilities.

Tata Ltd, one of the promoter companies of TCS, has sold its entire stake of 1.05% (1.03 crore shares) of TCS at Rs 615.04 per share in the open market. This sale of the stake will garner nearly Rs 650 crore. With this deal, Tata Group’s total shareholding in TCS had reduced to 75.16% from its earlier stake of 76.21% .

Telecom

The government has issued a service tax notice to Vodafone Essar Ltd. on account of evading service tax of Rs 3.67 crore. The company is liable to pay service tax for receiving services from foreign service providers as well as its distribution of the prepaid vouchers to its retailers and distributors in lieu of commissions for services rendered by them to the company.

|

Macroeconomic Indicators |

|

Table

1 : Index Numbers of Industrial Production (1993-94 =100) |

|

Table

2 : Production in Infrastructure Industries (Physical Output Series) |

| Table 3: Procurment, Offtake and Stock of foodgrains |

|

Table

4: Index Numbers of Wholesale Prices (1993-94 = 100) |

|

Table

5 : Cost of Living Indices |

|

Table

6 : Budgetary Position of Government of India |

|

Table

7 : Government Borrowing Programmes and Performance |

|

Table

8 : Scheduled Commercial Banks -

Business |

|

Table

9 : Money Stock : components and Sources |

|

Table 10 : Reserve Money : Components and Sources |

|

Table

11 : Average Daily Turnover in Call Money Market |

|

Table

12 : Assistance Sanctioned and Disbursed by All-India Financial

Institutions |

|

Table

13 : Capital Market |

|

Table

14 : Foreign Trade |

|

Table 15 : India's Overall Balance of Payments |

|

Table

16 : Foreign Investment Inflows |

| Table 17 : Foreign Collaboration Approvals (Route-Wise) |

| Table 18 : Year-Wise (Route-Wise) Actual Inflows of Foreign Direct Investment (FDI/NRI) |

|

Table

19 : NRI Deposits - Outstandings |

|

Table

20 : Foreign Exchange Reserves |

|

Table 21 : Indices REER and NEER of the Indian Rupee |

|

Table

22 : Turnover in Foreign Exchange Market |

| Table 23 : India's Template on International Reserves and Foreign Currency Liquidity [As reported under the IMFs special data dissemination standards (SDDS) |

| Table 24 : Settlement Volume and Netting Factor for Government Securities Transactions Settled at CCIL - Monthly, Quarterly and Annual Basis. |

| Table 25 : Inter-Catasegory Distribution of All Types of Trade in Government Securities Settled at CCIL (With Market Share in Respective Trade Types) |

| Table 26 : Settlement Volume and Netting Factor for Total Forex Transactions Settled at CCIL - Monthly, Quarterly and Annual Basis. |

| Table 27 : Inter-Category Distribution of Total Foreign Exchange Transactions Settled at CCIL (With Market Share in Respective Trade Types) |

|

Memorandum Items |

*These statistics and the accompanying review are a product arising from the work undertaken under the joint ICICI research centre.org-EPWRF Data Base Project.

We will be grateful if you could kindly send us your feed back at epwrf@vsnl.com