|

Current Economic Statistics and Review For the

Week | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Turnover in India’s Foreign Exchange Market: A Review

The background In the strategy of economic liberalisation, the most dominant aspect has been the external sector liberalisation and it has taken manifold dimensions. Apart from the liberalisation of export-import trade, regulations regarding other current receipts and payments were rapidly relaxed such that early on after reforms India could opt for the system of current account convertibility for the rupee in 1994 under Article VIII obligations of the International Monetary Fund (IMF). Even capital account transactions were substantially liberalised with India’s position being described by some as de facto full capital account convertibility for non-residents and calibrated freeing of capital account transactions for residents. The results of the external sector liberalisation have been reflected in the enormous growth in the relative importance of external receipts and payments – current as well as capital. As shown in Table 1, the combined current receipts and payments, which had constituted 19.2% in 1990-91 and 25.2% of GDP in 2001-02, have shot up to 53.2% of GDP by 2007-08. Likewise, capital inflows and outflows to GDP ratios together have touched 63.8% against 12.2-16.4% earlier.

Associated with these facets of external sector liberalisation has been the enormous amount of flexibility provided to banks and other market participants to undertake foreign exchange operations and to manage their risks albeit gradually over time. In fact, in the foreign exchange market, there have occurred far reaching changes with a phased but quick transition from a pegged exchange rate regime for the rupee to a market-determined exchange rate regime in 1993. Simplification of procedures and introduction of new instruments such as forwards, swaps and options, have expanded the scope of liquidity in the forex market. As a result, the turnover in the country’s forex market has galloped in recent years (more on it later). The recommendations of the Expert Group on Foreign Exchange Market (popularly known as Sodhani Committee) towards the end of 1994 were a landmark in the design of foreign exchange market structure in India. Most of its recommendations were accepted and implemented. Some of the far reaching recommendations of the Committee were: (i) banks may be permitted to initiate cross currency positions overseas; (ii) they may be permitted to borrow and lend in overseas markets within prescribed limits; (iii) the number of market participants should be increased by permitting the then financial institutions like IDBI, IFCI to operate in the market; and (iv) corporates should be allowed to hedge, based on their underlying exposures. Thereafter, from time to time, a number of other and more dynamic liberalisation measures have also been introduced.

Jump in World Forex Market Share Before we present the extent and nature of growth in India’s foreign exchange market, an interesting revelation brought out by the Bank for International Settlements (BIS) from its ‘Triennial Central Bank Survey of Foreign Exchange and Derivatives Market Activity’ is worth noting. The results of the latest survey for April 2007 tell us that the growth in India’s foreign exchange market turnover has been the fastest between April 2004 and April 2007 amongst all reporting countries (see Table 2). While we must note at once that India’s share in the global forex market turnover is miniscule and still below 1%, it is the rapid increase in this share between 2004 and 2007 that was most striking. This share has tripled from 0.3% in 2004 to 0.9% in 2007. Also, more noteworthy is the fact that India’s share at 0.9% of the global total has overtaken the individual shares of all other important emerging market economies (EMEs) including South Korea (0.8%) and Mexico (0.4%); it has touched the share of Italy (0.9%), one of the G-7 economies. India’s performance has been all the more creditable because it has thus outperformed even the fast- growing emerging market currencies as a group. It is estimated that the total share of these EMEs in April 2007 was 20% of all transactions as compared to less than 15% in April 2004 or near 17% in 2001.

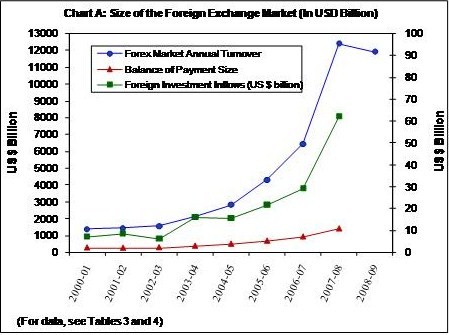

Much Faster Increases in India’s Forex Turnover in Recent Years Reverting to the growth in forex market turnover in India, the tempo of activity at a heightened pace began in 2003-04 or thereabout when the size of the country’s balance of payments (BoP) representing the sum total of current and capital receipts began to expand at a steady pace (Table 3). Apart from the pickup in merchandise trade, invisible receipts including private transfers have registered sizeable increases. More importantly, as shown in Table 4, capital flows have experienced a quantum leap in 2003-04 and have kept on increasing thereafter rather rapidly. This has been the time when the EMEs regained their importance after their sufferance from the impact of the Asian Crisis in 1997 which had given rise to a temporary halt to their capital inflows.

The increased tempo of external transactions, combined with liberalised arrangements for trading and settlement, has contributed to a still more rapid growth of turnover in the domestic forex market. As shown in Table 3 above, forex market turnover expanded near seven-fold between 2002-03 and 2007-08, while the BoP size increased four-fold. Alternatively, the forex turnover increased from 5.8 times the size of India’s BoP in 2002-03 to 8.8 times in 2007-08.

Looking at the turnover figures themselves (Table 5), what was a level of $1,560 billion in 2002-03 shot up near 8-fold to $11,928 billion in 2008-09. Likewise, the average daily turnover has bulged from $6.31 billion to $46.87 billion during the same period. These are no doubt crude numbers without taking into account exchange rate changes or changes in price levels; even so the broad theme of fast growth in forex transactions is self-evident. Within the overall forex market turnover, increased liquidity is getting reflected in a number of indicators. On the face of it, inter-bank turnover as a multiple of merchant transactions has been slightly edging down from above 4.0 in the second half of the 1990s to around 3.0 in the next decade (Table 6). But, this has happened because, with the availability of better instruments to protect their exposure, merchant transactions themselves now have a higher proportion of forward support. Thus, in merchant transactions, spot turnover had worked out to 63% during 2001-02, but thereafter it has steadily declined to 38% by 2008-09. On the other hand, in inter-bank transactions, the position has been somewhat the reverse (Table 7).

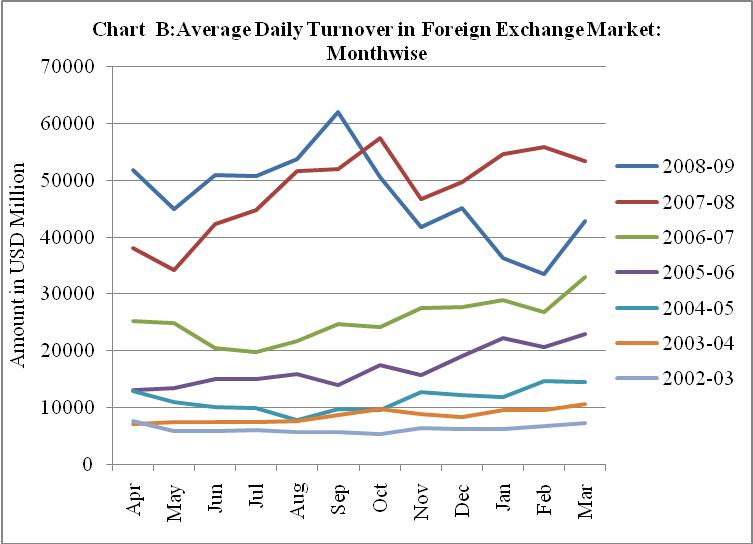

Overall, the data suggest (i) growing amount of forex market turnover as a multiple of the BoP size; and (ii) within the forex market turnover, a complex set of arrangements exists for the availability of increased liquidity, whether for merchant or inter-bank transactions. Seasonality and Halt to Growth in Forex Turnover in the Second Half of 2008-09 – Impact of Global Crisis With a view studying the seasonal behaviour of forex market turnover however crudely, we have depicted the monthly figures of average daily transactions in Table 8 and Chart B. It is found that in the ongoing phase of rising forex transactions beginning with the year 2002-03, the average daily turnover has been generally consistently showing an upward trend from month to month, with every year beginning with the lowest number and the numbers for the final January-March quarter being the highest in each of the years studied except the latest year 2008-09.

The consequences of these adverse external accounts situation are found in a steep decline in forex turnover almost every month as compared with the previous month – and rather more steeply as compared with the previous year. Broadly, the average daily turnover in the second half of 2008-09 has been about 20% lower than the average daily turnover in the first half of the year which has happened almost for the first time probably in over a decade. Also, as shown in Appendices A and B, the decline in total as well as average daily turnover has occurred in successive quarters of the year. To an extent, as cited earlier, this may be due to the appreciation of the US dollar even in the current situation of global crisis faced by the US economy. (The statistical tables and graphs for this note have been prepared by Mrs. Anita B. Shetty)

Highlights of Current Economic Scene

Agriculture The central government is unlikely to relax the export ban on both staple foodgrains (Wheat and Rice), in spite of record procurement undertaken since last two years. The government has plans to use these stocks to fulfill the promise made by the congress party for providing subsidised grain to the people living below poverty line. The central government has recommended a technical group to revise the buffer norms for rice and wheat in a month's time to maintain food security, on account of record procurement of foodgrains during this year, i.e. around 565 lakh tonnes. Of which wheat and rice would be around 240 lakh tonnes and 310 lakh tonnes, respectively, while remaining 15 lakh tonnes are in the form of coarse grains such as jowar and bajra. The state government of Maharashtra has targeted to produce 92.5 lakh tonnes of foodgrain by covering the acreage of 147 lakh hectares under sowing during the ensuing kharif season of 2009. In 2008-09 sowing took place on 133.2 lakh hectares of land as against the average sowing area of 134.2 lakh hectares, while production of pulses (-28%), cereals (-54%) and oilseeds (-51%) slipped down drastically. Production of important kharif crops like rice and jowar decline by about 7 lakh tonnes each, while bajra production was lower by 4.4 lakh tonnes. This poor performance was mainly due to the prolonged dry spell in the monsoon, the consequent late sowing and pest attack in vidarbha. So this year each farmer is crossing their fingers for good monsoon as only 16% of land is under irrigation and th remaining is entirely rainfed. According to president of Pulses Importers Association of India, coverage under kharif pulses would increase by 10% to 15% in 2009-10, as farmers are attracted to higher market prices. It is predicted that most of the farmers would opt for intercropping of pulses with cotton, soyabean and maize, as these would help them earn more. The government is likely to allow private sector trading firms like PEC, MMTC and STC as well as one PSU or notified agency in each state to export wheat products like atta, suji and maida while it has been restricting shipment of the grain for the three central public undertakings and one state level agency. Sugar mills from the country would reduce overseas purchases of raw sugar as global prices have suddenly increased. This would decline imports to 2.5 million metric tonnes by the year ending September 30 as against earlier estimates of 3 million tonnes. The Forward Market Commission (FMC) has suspended trading in sugar futures with immediate effect till 31 December 2009 due to rising international prices, lower domestic output during 2008-09 crushing season, inflationary pressure and lower output forecast for the new season beginning November 2009. Under advance license scheme (ALS), traders and mills are allowed to import raw sugar at zero duty when there is a shortage in the country with an obligation to export similar quantity of refined sugar within a prescribed period owing to which sugar exports is estimated to be at 137000 tonnes in the first six months of the 2008-09 season (October-September). India exported over 100,00 tonnes of sugar in the current season even as the government has allowed imports of 1 million tonnes at zero duty to increase domestic availability. According to the US Department of Agriculture's Economic Research Service, the acreage under soyabean are expected to increase by 2% to 98 lakh hectares as against last years rise of 9%. Moderate increases are reported on soyabean acreage during 2009-10 due to the pressure on farm prices exerted by large imports of vegetable oil and bumper domestic rapeseed crop. The rise in soyabean output could help to raise the oilmeal exports to 48 lakh tonnes from 40 lakh tonnes this year. Soyabean production is expected to be up by 14% to 241.7 million tonnes with most of the increase is likely from other countries instead of US. Increase in coverage under soyabean worldwide, would make up the entire increase in global oilseeds production to 259 lakh tonnes, offsetting a projected decline in rapeseed, sunflower, cotton and groundnut. As per the report by Indian Maize Development Association (IMDA), country is estimated to generate an annual demand of nearly 23 million tonnes of corn by 2011-12, out of which 19.66 million tonnes would be for non-food uses like poultry and cattle feed. Total production of maize is estimated to rise to 42 million tonnes in 2025 from a projected 22 million tonnes in 2010, if the output increases by 6-7 million tonnes in every five year. Cotton Association of India (CAI) reiterated that most of the farmers are likely to opt for cotton production, after benefiting from high prices last year. Cotton sowing has started in some north Indian states like Punjab, Haryana and Rajasthan. Cotton cultivation in 2008-09 was around 9.2 million hectares, while there are possibilities that acreage in the country would jump to 9.5 million hectares in 2010. Cotton production in financial year 2009 is estimated to be lower at 290,000 bales as compared to 315,000 bales during the same period a year earlier. However, industry players estimate a crop of 340,000 bales in financial year 2010. According to study undertaken by Associated Chambers of Commerce and Industry of India (Assocham), improper use of pesticides by farmers have led to yearly crop losses exceeding Rs 1 lakh crore and also harming 20% of the agrarian land, which have irrigation facilities, in terms of yield and fertility. Farmers of Maharashtra requires 9 lakh tonnes of complex fertilisers for the kharif season 2009, but as there is short supply, it is predicted that farmers would get 4.50 lakh tonnes, owing to which state government has decided to ask the state run Maharashtra Agro-Industries Development Corporation (MAIDC) to provide complex fertilisers.

IndustryThe General Index (IIP) stands at 297.9, which is 2.3% lower as compared to the level in the month of March 2008. The cumulative growth for the period April-March 2008-09 stands at 2.4% over the corresponding period of the previous year. The annual growth of thee Indices of Industrial Production for the Mining, Manufacturing and Electricity sectors for the month of March 2009 at 0.4%, (-)3.3% and 6.3% as compared to March 2008. The cumulative growth during 2008-09 over the corresponding period of 2007-08 in the three sectors have been 2.3%, 2.3% and 2.8% respectively, which moved the overall growth in the General Index to 2.4%. In terms of industries, as many as five (5) out of the seventeen (17) industry groups (as per 2-digit NIC-1987) have shown positive growth during the month 2009 as compared to the corresponding month of the previous year. The industry group ‘Beverage etc’ have shown the highest growth of 15.1%, followed by 8.3% in ‘basic chemicals ’ and 6.6% in ‘Rubber and plastic products’. On the other hand, the industry group ‘Food Products’ have shown a negative growth of 35.8% followed by 25.1% in ‘Wood and Wood Products; Furniture and Fixtures‘ and 18.1% in ‘Leather and Leather Products’. As per Use-based classification, the Sectoral growth rates in March 2009 over 2008 are 1.4% in Basic goods, (-)8.2% in Capital goods and (-) 4.4% in Intermediate goods. The Consumer durables and Consumer non-durables have recorded growth of 8.3% and (-) 3.4% respectively, with the overall growth in Consumer goods being negative at 0.8%..

InfrastructureThe Index of Six core industries having a combined weight of 26.7 per cent in the Index of Industrial Production (IIP) with base 1993-94 stood at 270.3(provisional) in March 2009 and registered a growth of 2.9% (provisional) compared to a growth of 2.9% in March 2008. During April-March 2008-09, six core industries registered a growth of 2.7% (provisional) as against 5.9% during the corresponding period of the previous year. Crude Oil production registered a decline of (–)2.3% in March 2009 compared to a lower fall of (-)0.3% in March 2008. The Crude Oil production registered a growth of (-) 1.8 during April-March 2008-09 compared to 0.4% during the same period of 2007-08. Petroleum refinery production registered a growth of 3.3% (provisional) in March 2009 compared to growth of 0.1% in March 2008. The Petroleum refinery production registered a growth of 3.0%during April-March 2008-09 compared to 6.5% during the same period of 2007-08. Coal production registered a growth of 5.2% in March 2009 compared to growth rate of 9.3% in March 2008. Coal production grew by 8.1% during April-March 2008-09 compared to an increase of 6.0% during the same period of 2007-08. Electricity generation registered a growth of 5.9% (provisional) in March 2009 compared to a growth rate of 3.6% in March 2008. Electricity generation grew by 2.7% during April-March 2008-09 compared to 6.3% during the same period of 2007-08. Cement production registered a growth of 10.1% in March 2009 compared to 9.3% in March 2008. Cement Production grew by 7.5% during April-March 2008-09 compared to an increase of 8.1% during the same period of 2007-08. Finished (carbon) Steel production (weight of 5.13% in the IIP) registered a growth of (-)2.6%in March 2009 compared to (-)0.9% in March 2008. Finished (carbon) Steel production grew by 0.4% during April-March 2008-09 compared to an increase of 6.2% during the same period of 2007-08. InflationThe official Wholesale Price Index for 'All Commodities' (Base: 1993-94 = 100) for the week ended 16 May, 2009 rose by 0.1 percent. The annual rate of inflation, calculated on point to point basis, stood at 0.61% for the week ended 09/05/2009 as compared to 8.66% during the corresponding week of the previous year. The index for major group Primary articles witnessed a very marginal increase. The index for fuel, power ,light and lubricants rose by 0.1% mainly due to increase in the prices of aviation turbine fuel and furnace oil. The index for manufactured products gone-up by 0.1 percent to 203.5 from 203.3 for the previous week. The index for 'Food Products' group rose by 0.5%. due to higher prices of imported edible oil, rice bran oil etc. The final wholesale price index for ‘All Commodities’ (Base: 1993-94=100) revised upwards from 228.5 to 227.3 for the week 21 March 2009, and hence the annual rate of inflation based on final index, calculated on point to point basis, stood at0.84 % as compared to 0.31%.

Financial Market Developments Capital MarketsPrimary Market Mangalore-based private sector lender-Karnataka Bank, plans to seek shareholders’ nod to raise up to Rs 500 crore through a qualified institutional placement (QIP). A QIP is private placement of equity shares or securities convertible into equity by a listed company with qualified institutional buyers approved by the market regulator, the Securities and Exchange Board of India (SEBI). The bank is raising the money to strengthen its capital base and expand credit.

Secondary Market Key benchmark indices surged to 8-month high, extending gains for the twelth straight week, boosted by strong inflow from foreign funds and positive global cues. Further signs of recovery in domestic and global economy and anticipation of a strong push for economic reforms by the newly elected United Progressive Alliance (UPA) government strengthened the investors’ sentiments. On the back of higher government expenditure, India's economy expanded 5.8% in the fourth quarter ended March 2009. The GDP grew 6.7% in the year ended March 2009, slowing from 9% in the previous year. A leading indicator of German business activity rebounded in May 2009, hinting that the economic slump is easing, though the gain was less than expected. In Asia, Bank of Japan Governor Masaaki Shirakawa said the economy is likely to experience a mild recovery as exports and production improve. He, however, said the outlook on the economy remains fraught with considerable uncertainties. The market gained in 4 out of 5 trading sessions during the week. The BSE Sensex gained 730 points or 5.31% to 14,625. The BSE Small-Cap and BSE Mid-Cap indices outperformed the Sensex. The NSE Nifty jumped 210.45 points, or 4.96%, to end the week at 4449. Foreign institutional investors (FIIs) have invested almost $1 billion during the week in May 2009 in Indian stocks with the overseas investors’ total inflows crossing the $4-billion mark in May this year. The net investment of foreign investors in the stocks of Indian companies stood at $4.2 billion with most of the inflows coming in May. Net inflows over the past 12 weeks have amounted to about $23 billion, equivalent to the levels seen in 2005 and 2006. The asset base of the mutual fund industry rose sharply in May and crossed the Rs 6 lakh crore-mark as equities surged and liquidity improved. According to data released by Association of Mutual Funds in India (AMFI) the assets under management (AUM) grew over 15% to Rs 6,37,609 crore from Rs 5,51,254 crore in April. This is the steepest monthly rise recorded since the market fall in January 2008. The equity asset base has, on an average, grown by around 25% in May and this is largely on the back of positive action in the equity markets. All the fund houses which have issued their AUM records for May reported asset growth. With a new government in place, the high-level co-ordination committee on financial markets met under the chairmanship of RBI governor D Subbarao on 30 May to have a pre-Budget deliberation. The meeting reviewed the developments in financial markets, developments in corporate bond market, regulatory issues relating to ULIPs and MFs and investment in security receipts issued by asset reconstruction companies.

Derivatives The market continued to register net gains through an extraordinary high volume settlement week. The Nifty rose an amazing 28% in May and it surged again on the first day of the June settlement. There was little profit-taking on 28 May but the trend got more bullish immediately post-settlement. Volumes remained consistently high and the daily volatility was quite high with the Nifty swinging through almost 4% daily. The Vix has settled down at about 40 after spiking to 90 in the post-election result stage. Premiums are almost uniformly high. Defying gravity, the market continued to witness a firm trend. The Nifty June future closed the week at 4441 with a gain of 4.8% over the previous week’s close of 4256.2. However, the June future closed at a discount of about eight points with respect to the spot close of 4448.9. Besides, June series saw a market wide rollover of 69%, which is significantly lower than the average 75% rollover witnessed over the past few months. Only 58-59% of the Nifty positions got rolled into the June series, which is also significantly less than the average 65% seen in the previous expiries. Volatility index witnessed large intra-day swings week. On couple of days, it crossed the 80-point mark during the trading session but closed sharply lower at 40.3 on 29 May against the previous week’s close of 83.7. A sharp rise in the lot value and an increase in derivatives margins are considered to be the main reasons for the huge volatility in the share market during the week. The cumulative FII positions as percentage of the total gross market position on the derivative segment as on 28 May declined to 41.75%. They were net sellers predominantly in recent times, particularly on stock and index futures. They now hold index futures worth Rs 11,451.4 crore (Rs 13,160 crore) and stock futures worth Rs Rs 18,577.7 croe (Rs 21,994.3 crore). On index options, FII holding decreased sharply to Rs 21,002.39 crore (Rs 38,040.58 crore).

Government Securities Market Primary Market Four state governments auctioned 10-year paper maturing in 2019 for the notified amount of Rs 4,500 crore on 26 May. The cut-off yield was set in the range of 7.44-7.53%, being lowest for Rajasthan and highest for Uttar Pradesh. On 27 May the RBI auctioned 91-day TBs and 182-day TBs for the notified amount of Rs 5,000 crore and 2,000 crore, respectively. The cut-off yield for the 91-day TB was set at 3.32% and for 182-day TB it was set at 3.59%. The RBI re-issued 7.59% 2016, 7.94% 2021, 8.24% 2027 and 7.40% 2035 government stocks for the notified amount of Rs 6,000 crore for the 7-year paper and Rs 3,000 crore each for the 12-year paper, 18-year paper and 26-year paper on 28 May 2009. The cut-off yield for these four securities was set 6.95%, 7.34%, 7.70% and 7.79%, respectively.

Secondary Market Government bonds had another bad week on back of concerns of increasing supply not being matched by an equivalent demand for debt securities. The yields on the benchmark 10-year paper climbed for a fifth week to end at 6.70% on Friday, after a finance ministry official said India may borrow more than planned in the first half of the fiscal year that started April 1.Bond yields headed northwards on stepped up government borrowings and credit demand revival from public sector petroleum refining companies. Traders said that hardening of yields was also partly on account of the Reserve Bank of India’s temporary retreat from open market operations (OMOs). The OMOs were conducted through buyback of certain categories of government securities. Last week, however, there were no OMOs in view of the comfortable liquidity. In addition, sale of debt securities by FIIs and some mutual funds pushed up yields. Foreign institutional investors sold about $558 million (about Rs 2,600 crore) of debt papers, mostly short and medium term government securities. Average daily trade volume was down to Rs 10,600 crore during the week, about Rs 600 crore decline over the previous week. But equity trade volumes jumped during the week largely triggered by the Participatory Note-driven FII inflows. Average daily equity trade volume amounted to Rs 22,369.07 crore on the NSE. Corporate debt trade volume though remained steady at Rs 600 crore, unchanged over the previous week. At the weekly liquidity adjustment facility (LAF) auction, the recourse to the reverse repurchase window of the RBI amounted to Rs 1,11,165 crore. In fact, throughout the week, recourse to the reverse repo window was above Rs 1 lakh crore. As per the RBI statement the government sold a planned Rs 6,000 crore of 7.59% notes due in 2016 at Rs 103.44 per 100-rupee face amount, or a yield of 6.9%. It sold Rs 3,000 crore each of 7.94% notes due in 2021 at Rs 104.73, giving a 7.3% yield, and 8.24% notes due in 2027 at Rs 105.15, a 7.7% yield. The government also sold Rs 3,000 crore of 7.4% bonds due in 2035 at Rs 95.66, or 7.7% yield. In a significant initiative that would further broaden securities trading in India, markets regulator Sebi has released the proposed framework for using wireless technology for such trades and has invited comments from market participants. Sebi has proposed extending the existing framework of Internet trading for the purpose, subject to security and encryption safeguards. Sebi-registered stock brokers who provided internet-based trading services would be eligible to provide the services using the wireless medium, subject to approval from the respective exchanges, said the statement. The market regulator said there should be secure access, end-to-end encryption and security of communication. Adequate steps would be taken for user identification, authentication and access control through means such as user IDs, passwords, smart cards and biometric devices to prevent misuse.

Bond Market During the week under review, 3 banks, 2 NBFCs and I corporate tapped the bond market to mobilize an amount of Rs 1,550 crore.

Foreign Exchange Market The rupee depreciated slightly to Rs 47.29 per dollar, down from the previous week’s level of Rs 47.19. The rupee rose to a one-week high on 29 May, capping its strongest month in more than a decade, on a surging share market and better-than-expected economic growth data. The local unit has risen 6.2% in May, its strongest monthly rise since at least the start of 1995. Near forwards softened slightly though far forwards remained firm. One, three, six and 12 month forward premia ended the week at 3.58% (3.78%), 3.52% (3.56%0, 3.03% (2.99%) and 2.51% (2.41%). Short forwards – cash to spot— widened to 2.26% (2.21%) in view of high interest differentials between the dollar and the rupee. Foreign banks returned to sell-buy swaps to take advantage of the RBI reverse repo rate of 3.25%. The fall in near forward premia also indicated that some inflows were in the offing. This also manifested in the Non-Deliverable Forward (NDF) market at Rs 47.30 (Rs 47.54). The dollar hit a five-month low against a basket of major currencies on the 29 May and the euro rose above $1.41 for the first time this year as investors bought higher-yielding currencies and assets on hopes of a global economic recovery. Sterling approached $1.62, almost an eight-month high, and capped its best month since 1985, while data showing the US economy shrank less than expected in the first quarter lifted global stocks. Concern about the expanding amount of debt needed to fund a record $1.8 trillion US budget deficit added to dollar woes the week and put the benchmark 10-year Treasury yield en route to its biggest two-month spike since 2004. Foreign exchange reserves have recorded their highest growth in more than a year in the week, following the general election results. Investment by foreign institutions in the stock market and an increase in the value of non-dollar assets have helped push up the value of forex reserves. According to RBI data, forex reserves, which include foreign currency assets, gold and drawing rights with the International Monetary Fund, rose $6.4 billion to touch $260.6 billion during the week ended May 22 — the highest weekly rise since April 2008.

Currency Derivatives The government has notified MCX Stock Exchange (MCX-SX), a part of Jignesh Shah-led group that also owns country's largest commodity bourse MCX, as a "recognized stock exchange", where trading would not be deemed as speculative transactions. Financial Technologies, had set up MCX-SX in October 2008 with the launch of trading in currency futures. Besides, MCX-SX also initiated trading in stock future and options contracts last year. The MCX SX June Rupee futures ended stronger at 47.25 on 29 May on reinforced expectations of increased capital inflows into equity markets. The rupee futures traded with an upward bias at 47.35. The rupee futures opened stronger at 47.60 and continued to trade with a strong bias at 47.53. Commodities Futures derivatives The commodity markets regulator, the Forward Markets Commission (FMC), has suspended trading in sugar futures with immediate effect on 26 May 2009. The commodity will remain suspended till 31 December 2009. The suspension of sugar futures trading is likely to hit the National Commodity & Derivatives Exchange (NCDEX), the country’s second largest commodity exchange, as the commodity was highly liquid on this platform. Sugar prices have plummeted anywhere between Rs 15 and Rs 30 per quintal countrywide after the futures-ban effected on 26 May. While in Delhi, wholesale price of the commodity plunged by Rs 30/qtl to the Rs 2,360-2,440/qtl level, in Mumbai, too, prices plunged. The price of S Grade sugar dipped by Rs 15/qtl to Rs 2,205/qtl whereas M Grade sugar price went down by Rs 20/qtl to Rs 2,250. Prices of the commodity are expected to go down further over the next week both on the spot and the futures market primarily on the back of rapid selling by traders immediately before and after the futures trade ban was imposed by the FMC. Deadline for foreign investors to bring down their holdings in commodity exchanges to below 5% has been extended by three months till 30 September. According to a statement released by the department of industrial policy and promotion (DIPP), holding more than 5% of equity in these exchanges after the deadline by a foreign investor or entity, including persons acting in concert, will be considered as a violation of the Foreign Exchange Management Act (FEMA). The move will give Goldman Sachs, Intercontinental Exchange (listed with the New York Stock Exchange) and Fidelity more time to comply with the new regulations. While Gold Sachs and Intercontinental hold 7% and 8% stakes, respectively, in NCDEX, Fidelity holds around 9% stake in Multi Commodities Exchange (MCX). On 26 May Singapore Commodity Exchange Limited (Sicom) and the NCDEX announced that they have signed an agreement for cooperation and the development of their commodity markets. This would make Sicom the first exchange outside India to trade NCDEX’s products and NCDEX the first exchange outside Singapore to trade Sicom’s products. The exchanges will designate new products to the cooperation in response to market demand and jointly promote these designated products. The proposed cooperation will enable designated products to be traded and cleared in both exchanges. In addition, NCDEX will make available its agricultural commodity index to Sicom to create derivative products. Wheat futures prices may continued to rule lower during the week mainly on restricted buying interest amid huge stocks with Food Corporation of India (FCI) and state government agencies. Wheat June 2009 futures on the NCDEX fell by nearly Rs 35 over eight trading session to trade at Rs 1,105 a quintal on limited buying support. On 27 May, prices quoted below Rs 1,100 mark a quintal. Crude oil futures on the national bourses gained further momentum on the weekend and prices rose nearly over 8% during the week on continued buying support from market participants mainly on reports of OPEC's decision to hold output and falling US crude reserves supported by dollar weakness. The gold futures on the MCX continued to rule higher during the week because of higher crude oil price supported by weak dollar value. MCX crude oil June futures crossed Rs 3,100-mark, up by nearly Rs 300 per barrel. The contracts were traded higher at Rs 3,119 per barrel on 29 May up by 8.14% over the previous week. Crude oil prices soared over $66 a barrel, approaching seven-month peaks as the US currency plunged to its lowest level against the euro so far this year. Dalian Commodity Exchange (DCE), China’s premier commodity exchange, launched the futures trading in polyvinyl chloride (PVC) on 25 May 2009. China Securities Regulatory Commission (CSRC) announced in mid-April its approval to launch PVC futures at the DCE. China is the world’s largest PVC manufacturer, with an annual output of 8.82 million tonnes last year.

Insurance The insurance regulator IRDA has stated that all health insurance products filed must allow entry at least till 65 years of age. Further it has clarified that any kind of difference in product specification for different age groups or for different entry age must be mentioned upfront in the prospectus and policy documents. In addition, Irda has announced that for each instance of delay in issue of identity cards to policyholders beyond 30 days from issue of policy may entail a penalty being levied on the concerned insurer. The insurance companies have to ensure adequate dissemination of product information on all their health insurance products on their websites.

BankingHousing finance company, HDFC and LIC Housing Finance (LICHF) have increased the margin requirement on housing loans to 25%. HDFC has set the limit at 20% and LICHF has made it 25%. By doing so the housing financing companies (HFCs) have made owning a home difficult, as individuals availing housing finance has to contribute a higher sum from their own pockets. Banking analysts opined that the HFCs have raised the margin on account of higher risk weight on home loans. At present, the risk weight as is 75% on home loans up to Rs 20 lakh. The risk weight ranges from 50% – 100%, depending on the amount of loan.

Corporate Bharti Enterprises in partnership with the Singapore-based Del Monte Pacific has ventured into food and beverage products and is planning an investment of Rs 100 crore in the current fiscal year. The joint venture (JV) has launched a range of food and beverage products from Filipino-based Del Monte Pacific that includes fruit drinks, packaged fruits, ketchup and sauces, apart from several Italian products for the Indian market. The JV is also planning to set up a new facility near Hosur where production of fruit juice and other packaged food will start. Reliance Infrastructure Ltd has approved the capital infusion of Rs 4,300 crore in the company. As a result the promoter group’s holding will increase to 48% from 38%. This fresh equity infusion is proposed through a preferential offer of warrants to be converted into 42.9 million equity shares to promoters, LIC and other insurance companies. Tata Motors is likely to approach the existing consortium of banks, which have financed the $2.3 billion Jaguar and Land Rover (JLR) acquisition, for an extension of the due date on new terms and conditions. Around $1.9 billion still remains to be repaid of the $3-billion bridge loan raised by the company for the JLR acquisition which is due in June. SAIL has posted a dip of 37% in the fourth quarter ended March 31, 2009 to Rs 1,487 crore as compared to Rs 2,377 crore during the corresponding period last year. On account of slowdown in demand for steel coupled with high input costs the company’s net profit in the financial year 2008-09 declined by around 18% to Rs 6,175 crore from Rs 7,538 crore in 2007-08.

External SectorExports during April 2009 at US$ 10743 million which was one-third lower than that in April 2008 Imports during April were valued at US $ 15741 million, a decrease of 36.6 per cent over that of US$ 24823 million in April 2008.Thus the trade balance during the month worked out to be $ 5004 as compared to $8747. While oil imports was valued at $3634 million, that of non-oil imports was lower by 24.6% at $ 12113 million. Information TechnologyDuring the first quarter of the calendar year 2009, India’s personal computer (PC) market has recorded a 7% sequential growth in shipments on account of increased demand from the government, education and the banking sector. according to IDC’s Asia/Pacific Quarterly PC Tracker, a total of 1.67 million units of client PCs were shipped during the January-March quarter. The top three players in the India client PC market during the quarter were HP, HCL and Dell, respectively.

TelecomIndus Tower, an independent telecom tower company, has become the first ever company in the world to have the landmark of 1-lakh towers under its management. The company is a joint venture between Bharti Group, Vodafone Essar and Idea Cellular. Bharti group and Vodafone Essar each holds 42% stake, while Idea has the remaining 16% stake in the company. At present, Indus is having existence in 16 telecom circles throughout India. Sharing passive infrastructure is a new trend in the telecom sector as it enables the telecom operators to minimise their operating as well as capital expenditure. Bharti Airtel has re-initiated discussions to acquire a 49% stake in South Africa’s MTN for over $23 billion in cash and stock swap, after a year-long gap following the breakdown of negotiations between the two over the combined entity’s controlling structure. If the deal materialises, the combined entity would have 200 million users (with both partners contributing an equal 100 million each) – creating the world’s third-largest telecom company in terms of subscriber base after Vodafone Plc and China Mobile. Revenues of the combined entity would be around $20 billion. The potential deal would increase Bharti’s footprint to over 21 countries spanning South Africa and the Middle East, where the MTM currently operates services. At the moment, Bharti has an overseas presence in only three small countries, namely, Sri Lanka, the Seychelles and the Channel Islands. Tata Communications reported about Rs 9,963 crore in consolidated revenues for the year ended March 31, 2009 against Rs 8,297 crore in 2007-08, as per audited financial results under Indian GAAP. Net profit has increased to Rs 316 crore against Rs 10 crore in 2007-08, this included an extraordinary gain of Rs 286 crore (net of taxes) from the sale of shares in Tata Teleservices. Excluding the extraordinary gain the profit of the company has stood at Rs 30 crore – a rise of 200%. Reliance Communications (RCom), has received approval from its shareholders for the de-merger of its optic fibre division and subsequent merger with wholly owned subsidiary Reliance Infratel. The scheme is now subject to requisite approvals and sanctions, inter-alia of the Bombay High Court. Last week, the shareholders of Reliance Infratel had adjourned the meeting of its shareholders amid reports of minority shareholders raising objection to the scheme of consolidation of RCom's optic fibre division with itself. The de-merger will help reduce the set-up and operating costs resulting in cost efficiency. In addition, the segregation of business into providing telecommunications services and infrastructure will enable both the companies to concentrate on their core businesses.

*These statistics and the accompanying review are a product arising from the work undertaken under the joint ICICI research centre.org-EPWRF Data Base Project. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

We will be grateful if you could kindly send us your feed back at epwrf@vsnl.com | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

The latest year

2008-09 has a number of special features insofar as the external sector

transactions are concerned and these are directly related to the impact of

the global economic crisis faced by the economy. The economy has lost near

$58 billion of foreign exchange during the 12-month period of that year

(though to a sizeable extent due to valuation losses). Growth in

export-import trade has suffered a setback, with exports growth in dollar

terms dipping to 3.4% from 29% in the previous year and imports growth to

14.3% from 35.5%. The first three-quarter BoP data show substantial

declines in the growth of invisible receipts. More significantly, there

has occurred a sharp absolute decline in portfolio inflow during the year

(Table 9), though in the first two months of 2009-10, the trend has

reversed and the net FII inflows turned positive amounting to $5.7

billion.

The latest year

2008-09 has a number of special features insofar as the external sector

transactions are concerned and these are directly related to the impact of

the global economic crisis faced by the economy. The economy has lost near

$58 billion of foreign exchange during the 12-month period of that year

(though to a sizeable extent due to valuation losses). Growth in

export-import trade has suffered a setback, with exports growth in dollar

terms dipping to 3.4% from 29% in the previous year and imports growth to

14.3% from 35.5%. The first three-quarter BoP data show substantial

declines in the growth of invisible receipts. More significantly, there

has occurred a sharp absolute decline in portfolio inflow during the year

(Table 9), though in the first two months of 2009-10, the trend has

reversed and the net FII inflows turned positive amounting to $5.7

billion.